Get a call back!!

Get a call back!!

1800-12000-0055

Life sometimes brings unannounced uncertainties and hardships. Some events may have an irreparable impact on your life and may leave your family in a turmoil both financial and emotional. To reduce the financial worries that may erupt due to the unpredictable and untimely demise of the earning member of the family, the life insurance comes to the rescue. Life insurance is a vital form of investment that will act as financial aid or assistance to your family when you are not around.

Life insurance plans are of various types out of which a few plans are pure protection plans offering a death benefit, whereas the others are saving or investment plans offering death and maturity benefit (whichever occurs first).

Get QuotesLife Insurance is a long term contract (known as LIFE INSURANCE POLICY) between the Life Insurance Company (known as INSURER) and the person whose life is being insured (known as LIFE INSURED) for a specified tenure (known as POLICY TERM) giving an amount of money equal to the life cover (known as SUM ASSURED) by paying a cost (known as PREMIUM).

In the event of death of the Life Insured (known as DEATH CLAIM) during the policy term, the insurance company passes on the requisite amount as policy proceeds (known as DEATH CLAIM AMOUNT) to the specified family members (known as BENEFICIARY/NOMINEE) mentioned in the contract and the policy terminates thereafter or in the event of life insured survives through the policy term, the insurance company pays out the promised amount (known as MATURITY CLAIM AMOUNT) to the policyholder and the policy terminates thereafter.

Life Insurance primarily covers the risk of ‘Dying too early’ or ‘Living too long’. The listed reasons will highlight the need for life insurance for you and your family:

A life insurance policy assures that your loved ones are financially covered in the event of your untimely demise and to maintain the same lifestyle which they are used to even when you are not around.

A life insurance policy ensures that your children’s education, their marriage, and other financial obligations like home loans, car loans, etc. are taken care of in your absence.

A life insurance policy helps you to gather a corpus for your better future and to attain a regular source of income post-retirement and lead an independent life.

It helps you and your family to possess a guaranteed income in case your regular inflow of earnings are disrupted due to a severe illness or an accident.

A life insurance policy provides you the assured peace of mind. By buying the right life insurance plan, your family’s financial needs are taken care of even when you are not around.

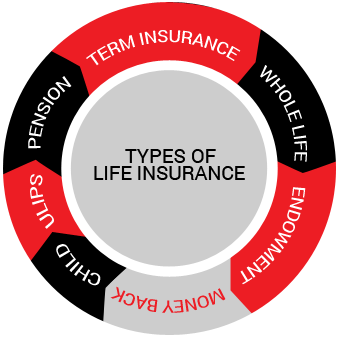

There is a bundle of life insurance plans available in the market. It purely depends on which one suits your need and requirement basis the benefits accrued or attached to a plan.

The term plan is a pure protection plan which covers the risk of ‘dying too early’. Term plans provide the nominee with the sum assured as a financial indemnification in the unfortunate event of your demise during the policy term and policy then terminates. A term insurance plan safeguards your loved ones in your absence by shielding them with financial backing as planned by you.

The whole life plan is an insurance plan which covers your life against the risk of “dying too early” and “living too long” both, as the life cover is provided for the whole life keeping maximum maturity age as 100 in most of the plans. This insurance company pays the policy proceeds to your nominee in the event of your death during a policy term, but if you survive till the maximum maturity age, the company will provide the maturity benefit as well.

Endowment plan comes with the component of saving and insurance making it a twin benefit plan under the policy. Endowment plans offer lump sum payout in the event of death or maturity, whichever happens first. This life insurance plan can be opted to ensure a robust corpus and regular savings to meet financial objectives in the future.

This policy offers a portion of the sum assured payout on regular intervals during the policy term in terms of money backs or survival benefits, while the insured is alive. Once the insured survives through the entire policy term, the remaining sum assured is paid back as maturity benefit. In case the insured dies during the term of the policy, apart from the money backs, the lump sum payout is given to the nominee also known as survival benefits.

Child plans are a type of life insurance plans, which are taken with a specific objective of giving unperturbed financial support to the child in terms of education, higher education, marriage, etc. Child plans also offer death and maturity benefits (whichever happens earlier). Usually, such plans come with an inbuilt waiver of premium benefit to continue the policy to ensure coverage for your child.

ULIPs (Unit Linked Insurance Plans) provide the twin benefit of insurance and investment opportunities under one umbrella. ULIPs are linked to the market, and the insured’s money is invested in various funds (based on equities, debts, government bonds) as per the risk-taking capacity of the insured. The lump-sum payout is given to the nominee in the event of death, and the entire value of the fund is given to the insured if he survives the policy term.

Such plans cover the risk of ‘Living too Long’. Pension plans enable to survive the same lifestyle and allow financial independence after the retirement age. Regular payment of premiums builds a financial corpus, which can be withdrawn partly and the remaining can be utilized to provide pensions to the insured as stated in the policy.

The Premium for your Life Insurance policy is calculated, basis the following factors:

Age plays the most imperative role in deciding the premium amount. For younger life premiums are low, and for older people premiums are high. The insurance companies underwrite the case basis the risk involved in the customer’s life as per the age. So, it’s prudent to buy life insurance at an early stage.

The higher life cover or Sum Assured policies will have a higher cost or premium amount to cover the risk by the insurer. However, some insurers offer you the discounts on premium for choosing the higher life cover.

Intake of cigarettes, tobacco, alcohol, and other nicotine products will attract high premiums as such products are harmful to health and elevate the risk of an individual’s life. So insurers cover high-risk lives by charging more premiums or may decline the proposal.

Your health status also determines the amount of premium to be paid by you towards your life insurance policy. In case you possess diabetes, high blood pressure, non-standard BMI, or suffering from some severe disease will attract a higher amount of premium as compared to other healthy life of your age.

As per statistics, women tend to live more than men. The life expectancy of women is higher, so the mortality component of the premium amount is lesser for women as compared to men when applying for a life insurance policy.

Your occupation also plays a crucial role in determining the premium amount. A risky occupation like people working in the mining industry, oil, and gas, fisheries or any other dangerous profession increases the premium amounts for your policy.

Riders are additional benefits attached to your base policy which will offer you enhanced benefits apart from your base policy. Various insurers offer multiple riders which can be attached with the main policy as per the policy conditions. Riders come with additional costs.

An additional death benefit is paid to your nominee apart from the base policy payout. The nominated beneficiary/ nominee can receive term rider sum assured if you have taken this rider to your base policy.

An additional death benefit is paid to your nominee apart from the base policy payout. The nominated beneficiary/ nominee can receive term rider sum assured if you have taken this rider to your base policy.

There are severe illnesses which disable an individual temporarily or permanently resulting in loss of earnings. The treatment cost of such illnesses is massive due to medical cost inflation. You can choose a critical illness rider to take care of the medical cost involved in such illnesses like Heart attack, Cancer, Paralysis, Coronary artery bypass surgery, Major organ transplant and many more.

As the name suggests, the future premiums are waived off in the events like death or disability of the insured or policyholder as per the policy contract. The policy continues to survive till the end with the waiver of future premiums.

Life Insurance benefits are usually given to the nominee/s as a one-time lump sum, and income benefit rider allows your nominee to receive the policy benefits in installments as a regular income. This rider allows you to regulate the dispersal plan of policy proceeds that suits best for your family in your absence.

Disability rider replaces your income for the specified tenure in the event of permanent or temporary total or partial disability due to an accident. The payout varies with the kind of disability occurred and also basis the insurer’s rider conditions. In case of total disability, the payout is the full sum assured whereas, in case of partial disability, the payout is the partial sum assured.

(Note: The rider benefit, conditions, and eligibility criteria may vary from insurer to insurer.)

Get QuotesYour life insurance plan excludes the following:

This clause states that the policy benefits are paid out only in the event where the life insured is killed in a commercial plane crash while traveling. But if the life insured dies as a passenger in a private plane insurance company will not entertain the claim.

This exclusion says that in the event the death of the life insured happens due to the involvement in certain dangerous adventure activities like auto racing, rock climbing, hang-gliding, etc., the payment of the policy proceeds will not be paid.Some insurer’s cover death arising out of such activities at a very high premium rate.

This exclusion provides that the insurer will not pay if the cause of death is a result of the war.

Read the do’s and dont’s related to your Life Insurance Plan.

| Do’s | Dont’s |

| Assess your needs and requirements in order to buy the right sum assured and right plan type | Ask your agent to fill the proposal form |

| Compare,choose and buy the plans online and save on cost | Leave any column blank in the proposal form |

| Fill the proposal form yourself.Mention the complete and corr ct details in the form | Conceal and misrepresent the facts, as it could lead to disputes during the time of claim settlement |

| Retain a copy of your duly filled proposal form for your own records | Make payment in the name of your agent advisor rather it has to be done in the insurer’s name |

| Read the fine print thoroughly before making payment | Buy a life insurance policy without comparing online |

Q: What is life insurance?

Ans: Life insurance provides the life cover and it assures you to pay the chosen sum assured amount to your nominee/ beneficiary in the event of your demise during the time policy is in active state. Life insurance is considered as the most economical way to secure the future of your family when you are not around.

Q: How a life insurance policy works?

Ans: A life insurance policy offers the cover against the life-related uncertainties. In the event of your unfortunate death during the coverage term, the insurance company will pay the sum assured amount to your nominee which ensures a comprehensive financial protection for your family.

Q: Do I really need life insurance?

Ans: You need life insurance, if any of the family members would be put at risk or suffer financially in the event of your death. If there are family members who are financially dependent on you, it is extremely essential to buy life insurance with a comprehensive cover.

Q: Which life insurance is best?

Ans: The motor insurance premium is calculated on the basis of some key factors like IDVWhen you are seeking to buy the best life insurance policy for you & your family, you firstly need to assess the future financial needs of your family and then pick the coverage accordingly. Also, check whether you need only the life coverage or looking for maturity benefit that will help to pick the life insurance policy such as term insurance, endowment, money back, etc.

Q: How much cover amount under life insurance is sufficient for my family?

Ans: When you are seeking to get the right life cover for your family to ensure they can lead a decent lifestyle even after your demise, you are advised to identify your family’s financial needs and then pick a life insurance cover accordingly.

Q: What are the benefits of having a life insurance policy?

Ans: Upon buying a life insurance policy, you will be entitled to receive the following benefits.

Q: What kinds of deaths are covered under life insurance?

Ans: Following are the types of deaths that are covered under a life insurance policy.

Q: What are the tax benefits for buying a life insurance policy?

Ans: Premium paid towards a life insurance policy taken for yourself, spouse or kids avail tax benefits under section 80C, and the benefits payable under the insurance policy are tax-free as per section 10(10D) of the Income Tax Act,1961.

Q: For how long should I continue the life coverage?

Ans: Life insurance provides coverage against the life risk and you should continue the life insurance coverage for at least 65 years of age. Although, the time duration till you need the coverage may vary depends on the circumstances and responsibilities that you have.

Q: What are the exclusions in a life insurance plan?

Ans: There are some exclusions for which an insurance company will not cover under a life insurance plan.