Get a call back!!

Get a call back!!

1800-12000-0055

A Unit Linked Insurance Plan (ULIP) is a life insurance product that offers the investment option along with a life cover. In ULIPs, your premium amount is allocated for both the investment element and the life cover. With investment options in ULIPs, you get the chance to grow your savings by investing in one of the fund options provided by the insurer and value of your investment also differs with the performance of your chosen fund. You can also choose an appropriate life cover as per the specific needs and choices. It is a market linked product and the risks associated with the investment are to be borne by the policyholder. Choose from a variety of unit linked insurance plans to suit your goals.

Get QuotesFollowing are the top reasons to buy a unit linked insurance plan.

In the present age of uncertainty, everyone likes to grow their money that can help them get through the tough financial times or lead a good life. Buying a ULIP plan ensures you higher returns depending on the performance of the fund, you have invested in.

Fulfilling financial obligations at different stages of your life is quite imperative. A ULIP plan helps you to easily achieve the goal-based savings and help you fulfill major financial obligations planned at different life stages.

Life is unpredictable and uncertain, and thus you need to ensure the financial protection for your family when you are not there. A ULIP plan offers life cover and pays a sum assured amount to the family/nominee in case of the demise of the life insured during the policy period.

As you are provided with several fund choices, you can choose a high performing fund to invest your money, and you get the chance to achieve higher returns. You only need to choose a fund option as per your risk appetite and see your money grow.

In today’s scenario of hectic life, everyone wants to ensure the family’s happiness always. A ULIP Plan provides life cover plus investment option to grow your wealth. It carries the dual benefits and thus assures peace of mind.

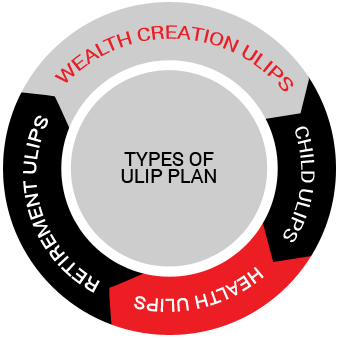

If you are looking to buy a plan that helps you build the wealth along with the insurance benefit, investing with a wealth creation plan is the best bet. This kind of unit linked plan helps fulfill your long-term financial goals with the life cover. Choose a wealth creation ULIP plan and obtain huge returns on your invested amount as per your risk appetite.

This type of unit linked plan aims to cater the financial needs for your child’s future, and it helps to manage expenses such as a child’s education, higher education, and marriage. By investing in this plan, your child can easily realize his dreams, even when you are not there.

This type of unit linked plan takes care of your health related expenses. In this plan, your premium amount is invested in a fund and thus provides the fund value and insure your health as well. It provides the dual benefits of health protection plus savings.

Everyone wants to save a huge corpus for their post-retirement period. Here is the market linked investment plan for retirement that helps you build a sum of money that you can withdraw as a lump sum and the remaining amount is used to purchase the annuities that you will receive for the rest of your life. These plans have different annuity options that you may opt for, as per your financial needs.

Following are the key factors that help determine the premium amount for the ULIP plan.

The age plays an important role in determining the premium amount charged towards the life cover for your unit linked insurance policy. If you buy the plan at an early age say at age 25, you need to pay the lower premium amount than the one buying at an advanced age say at age 40.The mortality cost is less for a 25 year old person as compared to a 40 year old.

If you consume alcohol, tobacco, and other nicotine products, your life is put at higher risk. Intake of these products is quite detrimental to health, and insurers tend to charge higher premiums to cover the increased life risk.

Your health condition also determines the premium to be paid by you for buying the life cover. If you suffer from any severe illnesses such as cancer, diabetes, or heart attack, you will be charged with the higher premiums in a ULIP Plan.

According to the recent statistics, men have lower life expectancy than women and thus have higher life risk. In order to provide the male policyholder a life cover, you need to pay the higher premium amount in a ULIP Plan.

The nature of your profession also affects the premium amount you pay towards the life cover in the policy. In case you are working in a high risk industry such as mining industry, Oil & gas, and fisheries, you are charged with the higher premiums.

Different insurers levy different charge structure when buying a ULIP. All the below mentioned charges are deducted from the premium amount for the policy and the remaining amount is then used for purchasing units in a ULIP. Following are the most important charges, you should be aware of.

These charges are deducted towards the cost incurred in servicing and maintaining the policy. These charges are deducted on a monthly basis and could be fixed for the entire policy period or may differ at a pre-specified rate.

These charges are deducted from the premium payment before allocating units under the ULIP. It includes initial expenses incurred by the insurer in issuing the policy, such as underwriting cost, medical expenses, and distributor’s fees.

These charges are levied on account of management of the fund(s). Fund management charges may vary for different funds. A fund with a higher equity element will be levied with a higher fund management charge.

These charges are levied by the insurer for providing the life cover to the policyholder. The mortality charges differ on the basis of numerous factors such as age, sum assured, prevailing health condition, etc. These charges are deducted on a monthly basis.

These charges are levied for either the premature partial or full encashment of units, as applicable in the policy terms. These charges are deducted as a percentage of the premium or the fund value.

You are provided with a limited number of fund switches in a year for free and upon exceeding that limit, Insurers charge a fee for switching between the fund options. Fund switching charges are levied on account of costs incurred in switching your funds.

Get QuotesFollowing are the key tips you may refer before buying a ULIP.

Prior to investing in a ULIP plan, it is important to assess your financial goals and then invest so that you can receive a huge amount on the maturity of the policy. You also need to plan your investment in a manner so that your policy matures and you can easily meet the financial obligations such as children’s education, marriage, etc.

A ULIP plan also covers the life risk that ensures financial protection for your family in case of your premature death during the policy period. While choosing the life cover, you also need to assess your financial obligations such as children’s education, marriage, or other day to day expenses of your family, so that the cover amount your family will receive can easily help them maintain the similar lifestyle.

Buying a ULIP plan early in your life helps you build a big fund value that you will receive at the maturity of the policy. Investing in the plan in the younger age also helps you get, the higher life cover at the low premium amount. Ulip’s are not an ideal plan for you if you are planning to buy it post touching 50 as high mortality charges will exhaust all the investment value.

There are a variety of funds to invest in as per the risk portfolio in a unit linked plan. It is important to choose the fund as per your risk taking capacity. In case you are well versed with market related investments and high risk taking appetite, then you may invest in equity based fund. But if you want a stable return, you may opt for a debt related fund or a balanced fund.

There are several charges involved when you invest in a unit linked plan and in order to get the best returns from the policy, it is recommended to invest for a long term (atleast for a minimum term of 10 years) which will help grow the fund value adequately.

Before buying a ULIP plan, it is recommended to compare the plans from different insurers and choose the one as per your and your family needs. You can also get the discounts on premium amount when buying a ULIP online.

Riders increase protection for your ULIP plan and all these are available at an additional cost. It would be a prudent decision to assess the benefits available with the riders and then attach the riders that suit to your needs.

It is recommended to read all about the policy terms & conditions, its benefits & exclusions. Read through the policy wordings which helps you assess whether the policy is a right fit for your needs or not.

Riders are add-on covers that provide additional enhanced protection. These riders are available at an extra cost and it’s recommended to assess the rider benefits before buying.

Following are the rider options to attach to your unit linked plan.

This optional rider covers the medical costs incurred due to severe illnesses such as a Heart attack, Cancer, Major organ transplant,etc. which may disable an individual that results in loss of earnings. Typically, the covered provided under this rider is the sum assured and paid additional to the sum assured in the base policy. The benefit under this rider is paid upon diagnosis of the illness.

This rider provides monthly income to the life insured in case of permanent or temporary total or partial disability arising due to an accident or illness. The payout differs and it depends on the kind of disability occurred.

This rider provides extra financial benefits to the nominee in case of death of the insured arising from an accident. The insurer pays the accidental death sum assured to the nominee, which is over & above the base sum assured of the policy.

This rider provides the death benefit to the nominee, which is additional to the base policy sum assured in the event of death of the life insured.

This rider waives off all the future premiums in the event of death or disability of the life insured. The policy continues till its maturity. It enables the policyholder to enjoy benefits of the insurance policy, even when they cannot work.

This rider provides the nominee/family of the life insured with the monthly income apart from the lump sum payout they get on the death of the insured. The payout and other benefits are subject to the terms mentioned specified the rider benefits.

This rider provides the policyholder an option to buy an additional coverage without any medical examination or any evidence about insurability. This rider is best for those who like to increase the cover at a later date on account of increased income and liability in the future.