Get a call back!!

Get a call back!!

1800-12000-0055

House provides shelter for living, and it is built upon the emotions and the efforts of the people residing in the house. Coming back to your house gives you a mental peace and warmth after a day's hard work. However, your home might be threatened with damages caused by natural and man-made calamities. Home is an asset, and you must secure it from any threat or damages. Home Insurance is a type of property insurance aimed to protect a home and its contents against damages. A Home Insurance policy provides financial protection in case of any damage happens to your home. A disaster may ruin your house, just buy a Home Insurance and get a cover for your home against losses/damages.

Get QuotesAny damage to your home could depress you both emotionally and financially, and that’s why you should seek cover to insure your home. Listed below are the top reasons to buy Home Insurance.

Nepal Earthquake and floods in southern part of India in the year 2015 took many lives; many homes were shattered and destroyed accounting it to an enormous financial loss.With a home insurance plan, you can keep your home protected against all types of ‘Natural disasters' such as earthquakes, cyclones, landslides, floods, and typhoons.

Despite installing security equipment and safety gadgets, man-made threats such as robberies, riots, strikes, thefts, and terrorism may pose the potential risks to your home. Although every insurer may not offer inbuilt protection against such events, you can ask them to cover against these damages as well.

Whether you are living in a housing society or renting your apartment, it would be a wise

decision to get your home insured. Buying a home insurance also protects your home

against fire and burglaries. Moreover, it also covers your personal ‘possessions' inside

your homes such as Household appliances, jewelry, a piece of art, paintings and other

valuables.

There are other structures that are a part of your home, but not attached to your homes

such as a garage or shed. By choosing the right home insurance plan, these parts of your

home can also be insured. Thus, by buying a home insurance plan, your home, and its

contents are completely secured.

A disastrous event may occur when a third party stays or visits your home. Few home insurance plans also offer the third party liability benefit that protects you against the legal liability that may arise due to damage or bodily injury to the third party.

Any damage or loss occurring to your house or contents in it, will prove disastrous. But with home insurance you have a financial assistance to deal with and an assured peace of mind in such scenarios.

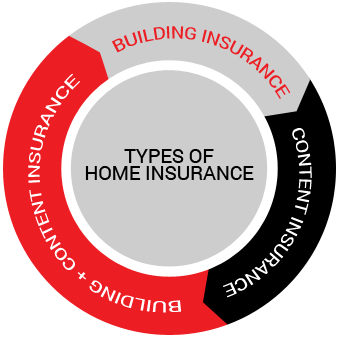

Following are the three most common types of Home Insurance Plans, you can choose from. The perils covered under the plans may vary from insurer to insurer.

This type of home insurance policy provides insurance cover to any the home structure or building against damage because of the man made purposes or natural calamities to the amount of providing claim for the full value of reconstruction in case of complete destruction or as per the defined terms and conditions in the policy.

This type of home insurance policy covers the contents of the house as they also hold a high value and any loss of such contents may result in a high financial loss. Content insurance pays for damage or loss of personal possessions located within the home. With contents insurance, the goods inside your house are covered against loss and damage caused by fire, flood, theft, or other perils mentioned in the policy. Contents may include important documents, jewelry, refrigerator, TV, piece of art, etc. are covered under this home insurance policy.

This is a comprehensive kind of home insurance policy which will provide protection against any damage which happens to the structure of home and also the valuable contents of your house.This kind of insurance cover provides a total protection to your home and will be a foolproof arrangement by providing financial assistance in terms of claim for any loss or damage due to the covered perils in your home insurance policy.

Following are the key factors that help compute the premium amount for home insurance.

While buying a home insurance, it needs to ensure whether you will insure the house structure, its contents, or both. If you insure both the structure of your home and its contents, you will be charged with the high premium amount.The more the scope of coverage, the higher is the premium.

Old homes are more susceptible to damage due to the wear and tear. Thus, old constructed houses attract the higher premium amount for a home insurance policy, whereas newly build properties are enhanced with several home protection measures will have lower premiums comparatively.

The cost of reconstruction will probably be more for a larger property, and so the cost of the reconstruction element goes up in home insurance. The higher cost of reconstruction also tends to increase the premium amount.

Location of your to be insured home is nestled at a high risk prone area for natural or man-made calamities, your insurer will charge the premiums at a higher rate.

The number of valuable items or contents you want to get it insured will attract higher premiums as the the sum at risk for the insurer will increase, and the insurer will cover the higher risk at an elevated premium amount.

Enabling high quality locks, smoke detectors, fire alarms, and burglar alarm will ensure more security of your home, so there are lesser chances of loss/damage to your property. Your insurer will then charge the premium amount at a lower rate.

If you opt for add-on covers such as cover for valuables, third-party liability cover, loss of rent, and burglary cover, it simply enhances protection for your home. Choosing add-on covers also attract additional premium amount as the scope of coverage is enhanced by opting for riders/add ons.

Voluntary excess in the amount of loss which the policyholder accepts to bear in case of a claim. It is the amount that policyholder pays towards a claim from his/her pocket. If you choose a higher voluntary excess, your insurer will charge lower premiums as part of the claim is shared between the policyholder and the insurer on the predefined amount or percentage.

A right home insurance policy provides cover against all eventualities. Nowadays, specific perils pose the potential threats to the safety of your home and its valuables. By opting add-on covers, you have the option to enhance the protection with your basic Home Insurance Policy.

Following are the key add-on covers, you can opt for:

This add-on cover protects your household items such as television, air conditioner, washing machine, refrigerator, and many more against loss or damage.

This add-on cover provides extra protection to your precious items such as important documents, jewelry, luxury watches, and much more against loss or damage.

This add-on cover provides cover against damage to the structure and/or its content caused due to burglary and theft.Some insurers offer it as an inbuilt cover, whereas with some of them offer it as an add on cover with the base home insurance policy.

Under this cover, the insurance plan covers loss or damage to the insured property due to earthquake or loss or damage due landslide or rockslide occurred, caused by the earthquake. It is an inbuilt cover with some policies, but also offered as an additional cover with the base policy.

This add-on cover provides protection to your house and its contents against the acts of terrorism. It’s a vital cover in today’s times of international disturbances.

If any loss/ damage caused to a third party or their property inside the insured’s home, then the third party liability arises to payoff for such damages. In this scenario, this home insurance policy pays for such damages.

This add on covers the death or bodily injury of the insured person by means of any accident or external force subject to the terms and conditions subject to the limits of the insurer’s liability.

This add-on cover provides protection for expenses towards rent for the time period you have to shift for repair work in your house or due to some calamity your house is damaged. The benefits under this cover is that the policy will cover the additional amount of rent during the specified scenarios.

(The add-on covers and its benefits may vary from insurer to insurer)

Get QuotesFollowing are the contingencies that are not included in the Home Insurance Plan:

• Willful destruction of property

• Loss or damage caused by wear & tear and/or depreciation

• Loss of property due to war/ nuclear war, act of foreign country, or invasion

• Loss of cash, antiques and collectibles

• Loss or damage caused to any electronic equipment owing to over-usage

• Loss or damage to property left unoccupied for more than a specified time period

Read the Do’s and Don’ts related to your Home Insurance.

| Do’s | Dont’s |

|---|---|

| Provide the complete and correct details, address and location of the house and contents for the evaluation in the proposal form | Conceal or misrepresent facts about the property & its fixtures in the proposal form |

| Have all the relevant documents ready and safe, to prove ownership and the value of the assets insured | Falsify the value of your property while tak ing a home insurance policy to seek lower premiums |

| Assess the premium rates from multiple insurers | Believe blindly on your insurer or intermediary. Research and get answers to all your queries |

| Take adequate Sum Assured to avoid low financial payout at the time of claim | Delay the decision of buying a home insurance if you possess high value content and property |

| Understand the technical jargons mentioned in your policy from an insurance expert to comprehend the benefits correctly | Assume everything is covered. Know about the plan exclusions in detail |