Get a call back!!

Get a call back!!

1800-12000-0055

A Car Insurance Plan provides cover against the financial risk that may occur due to the damage caused to the car. It covers damage when caused due to an accident, natural or man-made calamity. It also provides financial cover against the third-party liability that arises due to bodily injury/ property damage to a third party.

Get QuotesHere are some top reasons why you need to buy Car Insurance

Buying a car insurance in India is mandatory on the legal ground under Motor Vehicle Act, 1988. To drive a car on the road, you need to possess a valid insurance policy that provides a cover against third party damage at least.

If you have a car insurance policy, you don’t need to pay for damages caused to a third-party, when you are found guilty of. Your insurer will pay off for these damages subject to the terms of the insurance contract.

A comprehensive car insurance policy also pays for damages that are caused due to fire, theft, accident and natural calamities such as earthquake, flood, landslide, cyclone, etc. By purchasing a car insurance, comprehensive policy, you can claim the costly repairs for your car through your insurer. It also helps you to maintain the resale value of your vehicle.

By buying a car Insurance policy, you need not have to pay from your own pocket towards any third party liability or own damages. With a car insurance policy, you can get rid of any financial worries.

There are basically two types of Car Insurance Plans you can choose from.

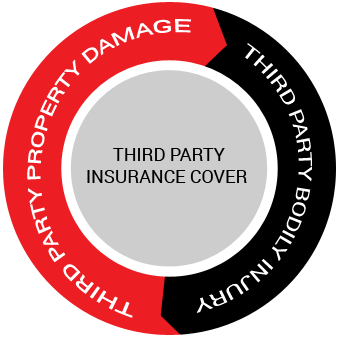

This policy provides cover against any legal liability that may arise due to damages caused to a third party (third party bodily injury or property damage) by your vehicle. Having a third party insurance is a legal requirement in India and administered under the Motor Vehicles Act. On the legal grounds, you need to carry a minimum third party car insurance cover damages caused to others. A third party insurance does not provide cover against damage to your own car. As it covers only the third party damage, the premium is also less as compared to a comprehensive insurance.

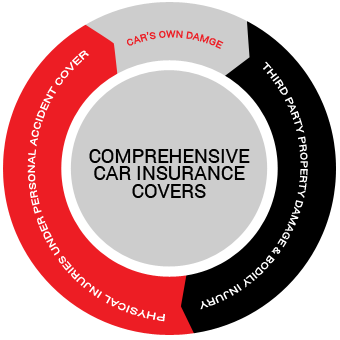

Unlike a third party insurance, a comprehensive car insurance offers three components under this kind of car insurance which are:

• Third Party Liability ( Which is mandatory by law)

• Own Damage (OD)

• Personal Accident Cover

Comprehensive Car Insurance provides cover against third property damage, bodily injury caused to a third party. Moreover, this car insurance also pays towards damage to your own vehicle which may be caused due to natural calamities such as fire, lightning, flood, hurricane, cyclone, hailstorm, explosion, inundation, frost, and landslide and man-made calamities which include burglary, theft, riot, etc. Also, this policy covers bodily injury to you as well under personal accident cover.

Several factors that help determine the premium amount for your Car Insurance are:

Your Insurance company may charge you the premium amount at a higher rate if your car has a higher value. Insured Declare Value (IDV) is a term that determines the value of your vehicle and deemed sum assured for your car insurance policy. The higher the IDV, more will be the premium amount. IDV is calculated on the foundation of the current day's showroom price of the car multiplied by the depreciation rate that is set by the TAC at the inception of each policy period.

Manufacturing year of the car and its registration date also plays a key role in determining the premium amount. For old cars, premium amount is lesser.Moreover, the vehicle’s expensive spare parts contribute to increase in the premium rate.

When opting for diesel, CNG or LPG based car, an insurance company will charge the premium amount at a higher rate compared to a petrol car. The reason being, diesel-run vehicles usually have higher usage and more wear & tear.

The premium amount of your car is based on the engine capacity of your vehicle. More the cubic capacity the higher will be the car insurance premium amount and vice versa.

Insurance companies have defined zones, each having a different rate of premium. There is Zone A (metro cities) and Zone B (rest of India). The registration location is taken into consideration while determining your insurance zone. If you have registered your car in Zone A, you need to pay higher premium compared to Zone B. These insurance zones are defined depending on the vulnerability of your vehicle to accidents and theft.

Car manufacturers nowadays are attentive to the safety of the passengers and thus, they equip cars with advanced and ultra-modern safety devices like advanced braking systems, robust locks, airbags, and anti-theft devices. Cars with more safety devices attract a discount on premium, thereby leading to a lower premium amount.

Various Add-on covers, you may opt from to avail enhanced protection to your car.

Depreciation is termed as a decrease in the value of the asset due to frequent usage. Your car is also an asset and is subject to depreciation. If opting for this cover, your insurer will provide a claim without deducting the depreciation amount on the value of parts replaced. This cover also provides cover against the repairing costs of glass, rubber parts, fibre, and plastic parts.

This add-on provides protection against damage to your car engine and electronic circuit caused due to flooding, or water logging. This cover helps you avoid huge repair costs, as your insurance company will pay off for the damages. It’s quite useful, especially during the monsoon season.

This add-on helps in saving your NCB upto one or two claims (depending on the insurer) during the policy period. It’s highly advisable to opt for this add on in case your accumulated NCB is above 25%.

There are stances when you have to face major issues in your car such as a mechanical breakdown. In this scenario, you don’t know how to resolve the car issue. With this add-on cover, you are provided with 24x7 roadside assistance to help resolve any mechanical issues with your car. This add-on is available at a nominal extra premium.

Long journeys in your own car with your loved ones are exciting. To protect your family or passengers in the car from any accidental expenditures, you may opt for this add on. Adding a passenger cover may slightly increase your premium.

This add-on enables you to claim for any apparent loss or theft of personal belongings such as an electronic equipment from a locked vehicle. The range of personal belonging, loss cover may differ from insurer to insurer.

In the case of medical emergencies, this rider pays for the ambulance charges and medical expenses that are incurred after the accident.

In case of car keys being misplaced or left in the car, key replacement cover efficiently assists you to unlock the vehicle in such scenarios. This add- on cover includes the cost of making a duplicate key if the key is lost and also the cost of lock if the lock needs to be replaced following the loss of a key.

(Note: The riders specified above may vary from insurer to insurer and can be bought by payng additional premium charges)

Get QuotesYour Car Insurance does not cover:

• Steady wear & tear.

• Loss/damage when driving under the influence of alcohol.

• Loss/damage when driving with an invalid driving license.

• Loss due to war, civil war, etc.

• Mechanical and electrical breakdown.

• Consequential loss.

• Claims that don’t include under the terms of the contract.

• Use of vehicle for any other purpose as mentioned under ‘limitations as to use’.

(Note: Read the policy terms of your car insurance to understand what is not included in your car plan.)

Read the Do’s and Dont’s related to your Car Insurance.

| Do’s | Dont’s |

|---|---|

| Compare car insurance plans online and avail discounts | Be forced to get the insurance from your vehicle dealer, you have the option to buy it online |

| Disclose all the information related to your car to the insured accurately | Choose too many riders or add ons. Excess of everything might not be beneficial |

| Read the fine print carefully | Let your No claim bonus affected for minor claims |

| Opt for riders prudently to enhance coverage | Forget to renew the policy after expiry of the policy period |

| Retain a copy of the duly filled proposal form for your own records | Undervalue your car to get a reduction in the premium. This may prove worse in times of claim. |